Have you ever wondered why banks seem to be everywhere? From your local neighborhood to the bustling city center, there is always a bank branch nearby. This widespread presence isn’t an accident. It is the backbone of a system known as Branch Banking.

But what exactly is it, and why does it still matter in an era of mobile apps and fintech? In this comprehensive guide, we will break down everything you need to know about branch banking, its history in India, its pros and cons, and how it differs from unit banking. READ here to explore Branch banking terms in detail and understand the financial ecosystem better.

What Is Branch Banking?

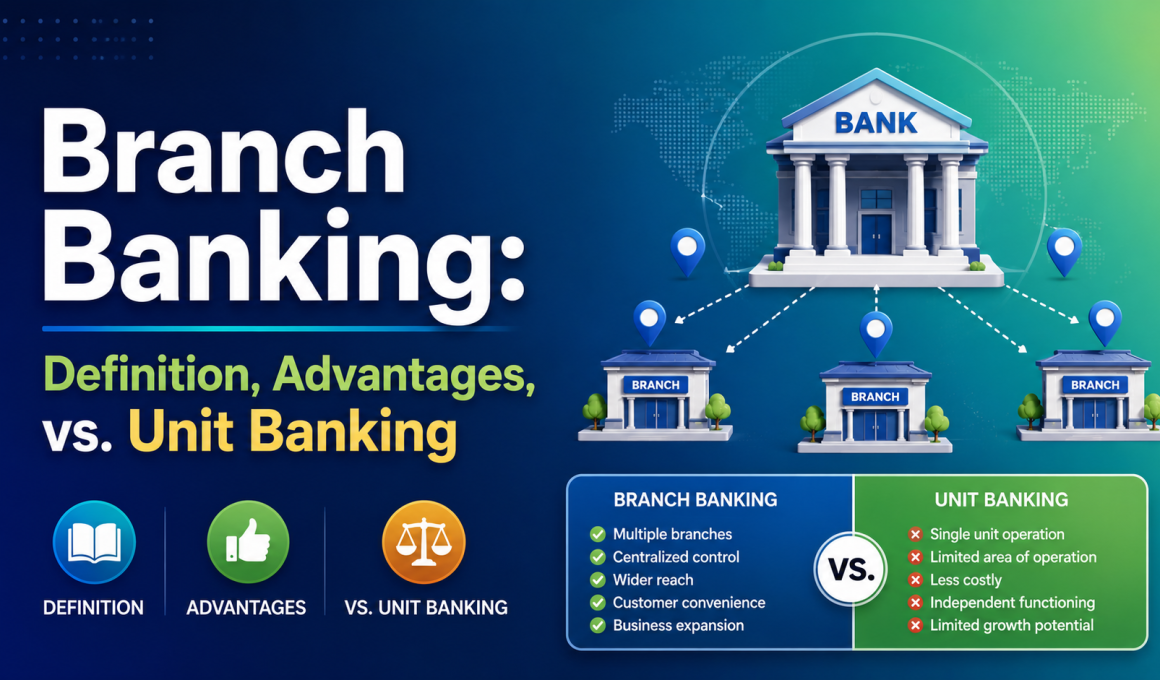

At its simplest, branch banking refers to a system where a bank operates multiple branches or offices in different locations to provide its services to customers. Unlike a single-office setup, this model allows a financial institution to have a physical footprint across various cities, towns, and even rural areas.

Think of it this way: If a bank decides to open five outlets in Mumbai alone, those are all branches connected to a central headquarters. When you visit any of these outlets, you are interacting with the same bank, accessing the same accounts, and utilizing the same security protocols.

This system makes banking easier by removing location barriers. For instance, Citibank started operations in New York in 1812. Today, thanks to the branch banking model, they have over 4,000 branches in 42 countries. This means a person traveling from India to the US can walk into a Citibank branch and manage their finances seamlessly.

Key Takeaways of Branch Banking

Before diving deep, here are the essential points you should remember:

- Network Presence: A branch banking system involves multiple office locations spread across geographies.

- Service Variety: Customers get access to deposits, loans, cash withdrawals, and personalized support.

- Indian Context: Banks like SBI expanded massively after nationalization to cover rural India.

- Modern Role: Despite digital growth, physical branches remain vital for complex transactions and trust.

- Challenges: High operational costs and management complexities are the trade-offs.

What Are The Functions Of Branch Banking?

Banks don’t just sit in buildings waiting for money to flow in. They perform specific roles to keep the economy moving. A typical branch banking outlet handles a variety of tasks designed to serve both individual customers and businesses.

Here are the primary functions you will encounter at most branches:

- Accepting Deposits: This is the most common activity. Branches collect savings, current, and fixed deposits. These funds become the capital the bank uses to lend to others.

- Lending Services: Banks provide loans such as personal loans, home loans, vehicle loans, and business financing. The branch evaluates your creditworthiness before approving the loan.

- Facilitating Withdrawals: Need cash? You can visit your local branch to withdraw money directly from your account, ensuring you have liquidity when you need it.

- Processing Payments: Beyond transfers, branches handle bill payments, utility charges, and other payment services securely.

- Customer Support: Sometimes, online chatbots aren’t enough. Branches provide face-to-face assistance with account queries, lost card replacements, and statements.

- Foreign Exchange Services: Major branches offer currency exchange for travelers and international banking services for exporters or importers.

- Opening New Accounts: Whether you want a savings account, a current account, or a demat account, the branch facilitates the KYC and paperwork process.

History and Current Landscape of Branch Banking In India

To truly appreciate the current state of banking, we must look at the past. Branch banking in India has a rich history that dates back to the colonial period, with the establishment of the first banks in the early 19th century.

One of the earliest milestones was the founding of the Bank of Calcutta in 1806, which eventually evolved into the State Bank of India (SBI). Over time, as the country grew, banks began expanding their presence through branch offices to serve India’s geographically dispersed population.

However, the landscape changed drastically in the post-independence era.

- Nationalization Era (1969): The Indian government nationalized 14 major private banks. The goal was to ensure more equitable financial services, especially in rural and remote areas where no bank wanted to go. This move marked a significant boost in branch banking, encouraging banks to open branches in previously unbanked regions.

- Liberalization (1991): The opening of India’s economy allowed new private sector players (like HDFC and ICICI) to enter the market. These banks used technology to rapidly expand their branch networks alongside public sector giants.

- Current Scenario: Today, policies by the Reserve Bank of India (RBI) focus heavily on financial inclusion. While internet banking is booming, the Pradhan Mantri Jan Dhan Yojana (PMJDY) scheme launched in 2014 reinforced the importance of branch banking. It enabled millions of unbanked individuals to open bank accounts with zero rupee deposits, often requiring a physical visit to verify identity.

Major players like SBI, HDFC, ICICI, and Punjab National Bank continue to maintain extensive networks. However, the integration of Core Banking Solutions (CBS) means customers can now perform transactions at any branch nationwide, not just the one where they opened the account.

Branch Banking Advantages And Disadvantages

Like any business model, branch banking comes with a set of benefits and drawbacks. Understanding these helps you decide when to use physical channels versus digital ones.

The Advantages

For customers, the biggest selling point is accessibility.

- Personal Touch: There is a level of trust built by speaking to a human being. Financial advisors in branches can help you navigate complex decisions like mortgages or retirement planning.

- Immediate Cash Access: No app can give you physical cash instantly. Branches handle large withdrawals or coin exchanges efficiently.

- Safety Deposit Boxes: Highly sensitive documents require the security only a physical vault within a branch can offer.

- Complex Transaction Handling: Things like fixing loan defaults, modifying property-related documentation, or dispute resolution are easier face-to-face.

Disadvantages Of Branch Banking

It isn’t all smooth sailing for the banks or sometimes the customer.

- High Operational Costs: Rent, electricity, staff salaries, and security for every single location make running a branch network very expensive.

- Management Challenges: Keeping thousands of branches uniform in service quality is difficult. Some branches may lag behind others due to staff turnover.

- Security Risks: With more branches comes more potential targets for fraud or physical robbery.

- Time Consumption: Queuing up at a branch during peak hours can waste valuable time, which is why many prefer online banking for simple tasks.

Branch Banking Vs. Unit Banking

People often confuse the two terms. To clear the air, let’s compare them side-by-side. While branch banking is about networks, unit banking is about isolation.

| Feature | Branch Banking | Unit Banking |

|---|---|---|

| Structure | Operates multiple branches across locations. | Operates only one office or branch. |

| Reach | Large, serving regional or national markets. | Small, limited to a specific locality. |

| Services | Wide range from basic savings to corporate loans. | Limited services due to fewer resources. |

| Risk | Risks are spread across multiple locations. | Higher risk as all capital is concentrated. |

| Decision Making | Centralized decisions from the Head Office. | Decisions made locally by the owner-manager. |

| Customer Interaction | Can be impersonal due to high volume. | Highly personalized relationships. |

As you can see, unit banking was common in older times or small rural areas, but modern economies rely on the scale and efficiency of branch banking.

Branch Banking Example

A perfect example of this system in action is the State Bank of India (SBI). As the largest public sector bank in India, SBI operates thousands of branches.

Imagine you live in a small town in Bihar. You walk into a local SBI branch to apply for a job loan. Even though the SBI headquarters is in Mumbai, that branch acts as an extension of the main bank. It accesses the same database, uses the same software, and follows the same compliance rules.

With the advent of Core Banking Systems (CBS), this example highlights a key feature of modern branch banking: Inter-operability. If you open an account at an SBI branch in Delhi, you do not lose access when you travel to Bangalore. You can withdraw money or update your passbook at the Bangalore branch because the data is centrally stored and accessible via the branch network.

This connectivity allows banks to reach millions of people across cities, semi-urban hubs, and deep rural areas, making financial inclusion possible on a massive scale.

Learn Banking With Wikitechy

If you find the world of finance fascinating, or if you are looking to build a robust career in this dynamic sector, knowledge is power. The banking industry is evolving rapidly, and understanding traditional models like branch banking alongside digital trends is crucial for professionals.

At Wikitechy, we offer specialized courses designed to prepare you for the modern banking landscape. Our BFSI (Banking, Financial Services, and Insurance) course provides in-depth knowledge of banking operations, soft skills, and interview preparation.

Whether you want to understand how core banking works, manage risk, or prepare for jobs in public and private sector banks, our experts can guide you. Completing the course provides you with an industry-recognized certification, helping you flaunt your portfolio on platforms like LinkedIn. Join us to gain practical insights and kickstart your journey into the financial services sector.

Conclusion

In summary, branch banking remains a cornerstone of the global financial system. While digital banking offers speed and convenience, the trust, security, and personalized touch offered by physical branches cannot be fully replaced. From the colonial roots in India to the digital integration of today, branch banking continues to adapt, ensuring that people from every corner of the country have access to essential financial tools.

Whether you are a customer deciding between an app or a counter, or a professional studying the banking sector, understanding the nuances of branches versus units, advantages, and functions is key. By balancing technology with physical presence, banks ensure a resilient financial ecosystem for everyone.

Branch Banking FAQs

1. Why do banks open multiple branches?

Banks open multiple branches to increase their market reach, offer services to customers in different geographic regions, and ensure that banking remains accessible to people living in rural or remote areas who may not use digital platforms frequently.

2. What services are available at branch banks?

Customers can expect a wide array of services including account opening, deposit collection, loan applications, cash withdrawals, foreign currency exchange, fixed deposit creation, and personalized financial advisory.

3. What are the disadvantages of branch banking?

The main downsides include high operational costs (rent, utilities, staffing), time delays due to queues, inconsistent service quality across different locations, and increased security risks compared to purely digital environments.

4. Can I access my account at any branch of my bank?

Yes, in most modern banking systems supported by Core Banking Solutions (CBS), you can access your account balance, transfer funds, or issue cheques at any branch of your bank nationwide, not just your home branch.

5. Is branch banking still relevant in the digital age?

Absolutely. While digital banking handles routine transactions, branch banking is still relevant for complex financial products, elderly customers who prefer face-to-face interaction, cash handling, and situations requiring immediate verification or physical documentation.

1. Why do banks open multiple branches?

Banks open multiple branches to increase their market reach, offer services to customers in different geographic regions, and ensure that banking remains accessible to people living in rural or remote areas who may not use digital platforms frequently.

2. What services are available at branch banks?

Customers can expect a wide array of services including account opening, deposit collection, loan applications, cash withdrawals, foreign currency exchange, fixed deposit creation, and personalized financial advisory

3. What are the disadvantages of branch banking?

The main downsides include high operational costs (rent, utilities, staffing), time delays due to queues, inconsistent service quality across different locations, and increased security risks compared to purely digital environments.

4. Can I access my account at any branch of my bank?

Yes, in most modern banking systems supported by Core Banking Solutions (CBS), you can access your account balance, transfer funds, or issue cheques at any branch of your bank nationwide, not just your home branch.

5. Is branch banking still relevant in the digital age?

Absolutely. While digital banking handles routine transactions, branch banking is still relevant for complex financial products, elderly customers who prefer face-to-face interaction, cash handling, and situations requiring immediate verification or physical documentation.